In 1900, there were just 8,000 automobiles registered in the United States.

By 1910, there were nearly half a million cars. By the start of the Great Depression in 1929 it had skyrocketed to 23 million.

Just 2% of households owned a car in 1910. By 1940, it was more than 90%.

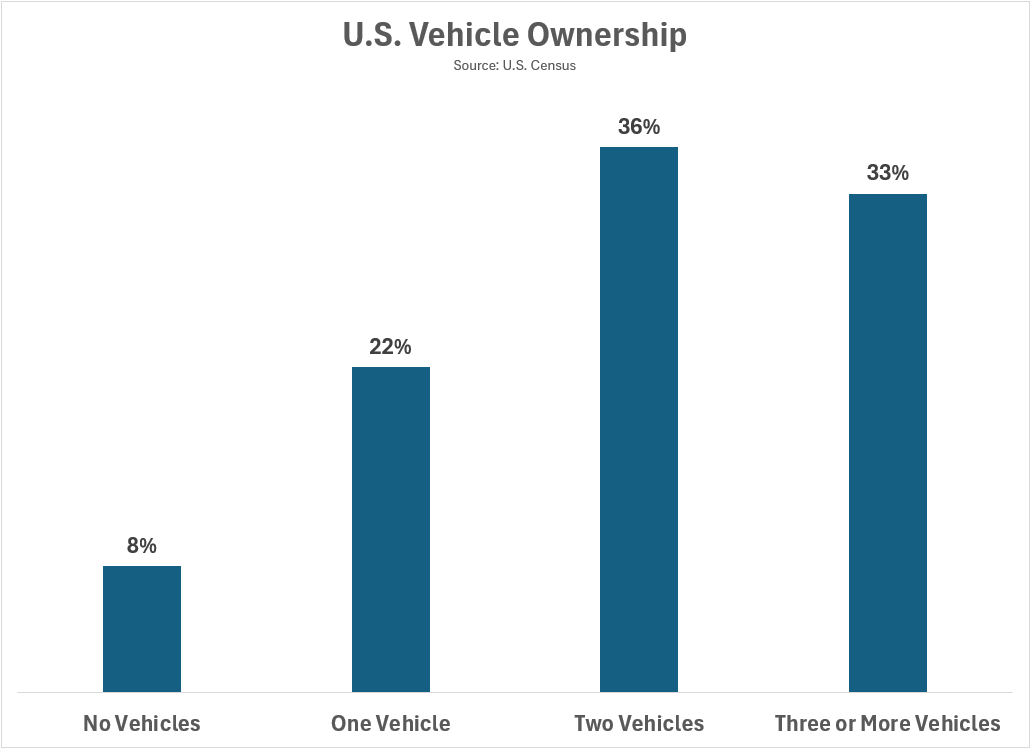

Today, 70% of U.S. households have access to two or more vehicles:

There were two main reasons vehicle ownership exploded higher in the early-20th century: (1) consumer credit and (2) the assembly line.

Most people couldn’t afford to buy a car with cash (which is still true today), so they financed it.

Henry Ford’s assembly line brought the cost of early models down considerably. According to Robert Gordon the cost of owning an automobile declined by 78% between 1912 and 1930.

Plus, the quality of the vehicles improved by leaps and bounds as well.

In the early 1900s, a doctor and his chauffeur were the first people to drive across the country successfully. They went from San Francisco to New York in 63 days in an uncovered car.1 By the 1940s, cars were enclosed, had much more powerful engines, improved transmissions, could go faster and you now had some highways to drive on.

The quality of vehicles continues to improve. We now have Apple CarPlay, navigation, rear cameras, all kinds of sensors, heated steering wheels, heated seats and self-driving capabilities.

Unfortunately, the costs are not falling now like they were back in the day.

Owning a vehicle is an expensive proposition that’s becoming increasingly more costly each year.

Here are stats and figures from a recent report by The Wall Street Journal:

- The total cost to own and operate an automobile averaged $12,296 in 2024 (30% higher than a decade ago)

- New-vehicle prices now average $48,883

- Used cars now average around $25,500

- Average insurance costs rose 10% in 2024, after soaring 15% in 2023

- Full-coverage auto policies now average $2,680 annually, up 12% from June 2024

- The average new vehicle loses $4,680 in value every year over the first five years

- In the last quarter 2024, one in four consumers were underwater on a car loan

- Garage repair costs are up over 43% in six years

- The average single repair across all types of vehicles was $838 in 2024

- The cost of fixing damaged cars has skyrocketed 28% since 2021

There’s a lot to digest but the one I want to focus on here is depreciation.

The average brand-new vehicle costs around $50k and depreciates by almost $5k a year in the first 5 years of ownership. That means the value of your automobile is essentially cut in half after 5 years.

Interestingly, the vehicles that lose their value the fastest tend to be the luxury brands2 that people pay up for:

It’s almost unfair to include vehicles in the same definition as actual financial assets.

Owning an automobile is a form of consumption.

It’s a necessary form of consumption for most people but the cost of ownership — insurance, repairs, maintenance, financing costs — have all gotten much worse this decade.

The cost of owning an automobile goes far beyond your monthly payment.

The good news is cars are lasting longer than ever before. The Journal notes the average age of passenger cars on the road today is 14.5 years.

Sticking with the same vehicle for a longer period is likely your best option for saving money on the cost of ownership.

And don’t buy a new car/truck/SUV if you can’t afford it.

Michael and I talked about car ownership costs and much more on this week’s Animal Spirits video:

[embed]https://www.youtube.com/watch?v=io627rzOgcc[/embed]

Subscribe to The Compound so you never miss an episode.

Further Reading:

Is Auto Insurance Becoming a Crisis?

84 Month Auto Loans?!

Now here’s what I’ve been reading lately:

Books:

1Interesting fact of the day — the first stop sign appeared in Detroit in 1915.

2Not all luxury brands. A Porsche tends to hold its value better than most cars.

This content, which contains security-related opinions and/or information, is provided for informational purposes only and should not be relied upon in any manner as professional advice, or an endorsement of any practices, products or services. There can be no guarantees or assurances that the views expressed here will be applicable for any particular facts or circumstances, and should not be relied upon in any manner.

You should consult your own advisers as to legal, business, tax, and other related matters concerning any investment.

The commentary in this “post” (including any related blog, podcasts, videos, and social media) reflects the personal opinions, viewpoints, and analyses of the Ritholtz Wealth Management employees providing such comments, and should not be regarded the views of Ritholtz Wealth Management LLC. or its respective affiliates or as a description of advisory services provided by Ritholtz Wealth Management or performance returns of any Ritholtz Wealth Management Investments client.

References to any securities or digital assets, or performance data, are for illustrative purposes only and do not constitute an investment recommendation or offer to provide investment advisory services. Charts and graphs provided within are for informational purposes solely and should not be relied upon when making any investment decision. Past performance is not indicative of future results. The content speaks only as of the date indicated.

Any projections, estimates, forecasts, targets, prospects, and/or opinions expressed in these materials are subject to change without notice and may differ or be contrary to opinions expressed by others.

The Compound Media, Inc., an affiliate of Ritholtz Wealth Management, receives payment from various entities for advertisements in affiliated podcasts, blogs and emails. Inclusion of such advertisements does not constitute or imply endorsement, sponsorship or recommendation thereof, or any affiliation therewith, by the Content Creator or by Ritholtz Wealth Management or any of its employees. Investments in securities involve the risk of loss. For additional advertisement disclaimers see here: https://www.ritholtzwealth.com/advertising-disclaimers

Please see disclosures here.

Disclaimer: This story is auto-aggregated by a computer program and has not been created or edited by finopulse.

Publisher: Source link