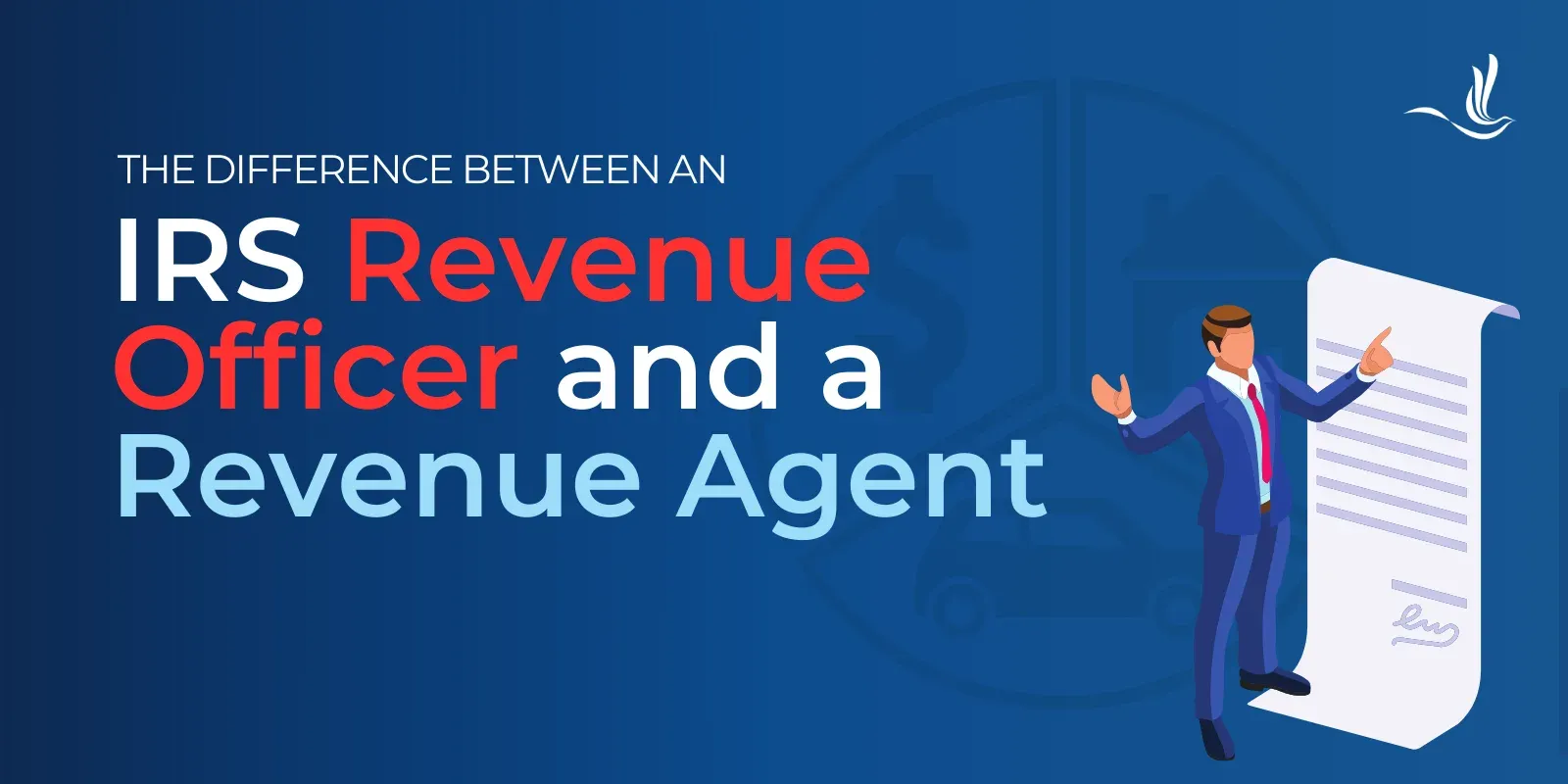

The IRS plays a critical role in ensuring that taxpayers comply with U.S. tax laws. Within the IRS, various professionals are tasked with different responsibilities, including revenue officers and revenue agents. While these roles may sound similar, they have distinct functions and purposes within the IRS. Understanding the difference between an IRS revenue officer and a revenue agent can be crucial for taxpayers who find themselves dealing with the agency.

IRS Revenue Officer vs Agent: A Quick Comparison

The main distinction between an officer and agent lies in their core focus:

- Revenue Officers collect taxes.

- Revenue Agents audit taxes.

Here’s a quick, side-by-side comparison:

FeatureRevenue OfficerRevenue AgentWhat They DoTax collection and enforcementTax auditing and compliance verificationAuthoritySignificant enforcement powers (levy, lien, seize)Audit and propose tax changes (assess penalties)Typical Interaction with TaxpayersDirect, face-to-face visits (sometimes confrontational)Audits (in-person, phone, or correspondence)GoalSecure payment of delinquent tax debtsVerify accuracy of filed tax returnsRole and Responsibilities

The true difference between an IRS revenue officer and a revenue agent lies within their roles and responsibilities.

Revenue Officer

A revenue officer is a field agent responsible for collecting unpaid taxes from individuals and businesses.

Their primary role involves enforcing tax laws and ensuring that taxpayers fulfill their obligations to pay taxes. Revenue officers are tasked with collecting delinquent tax debts and securing tax returns that have not been filed. They often work directly with taxpayers in person, visiting homes or businesses to resolve issues related to tax collection.

Key responsibilities of a revenue officer include:

- Collecting unpaid taxes and securing delinquent tax returns.

- Enforcing tax compliance through levies, liens, or seizures of assets.

- Working with taxpayers to set up payment plans or offer in compromise.

- Investigating and locating assets to satisfy tax debts.

- Ensuring that employers comply with employment tax requirements.

Revenue officers often handle more complex and severe cases where taxpayers have not responded to previous IRS notices or have significant unpaid tax liabilities. Their work can sometimes involve confrontation, as they have the authority to take drastic enforcement actions if necessary.

Revenue Agent

A revenue agent, on the other hand, is primarily focused on auditing taxpayers to ensure accurate reporting and compliance with tax laws. Unlike revenue officers, revenue agents do not focus on tax collection but rather on the verification of tax returns.

They conduct examinations of individual and business tax returns to determine if the reported income, expenses, and deductions are accurate and compliant with tax laws.

Key responsibilities of a revenue agent include:

- Conducting audits of individual and business tax returns.

- Reviewing financial records, books, and other documentation to verify tax return accuracy.

- Assessing additional taxes owed based on discrepancies found during audits.

- Providing guidance to taxpayers on how to correct errors and avoid future issues.

- Specializing in specific areas of tax law, such as international taxation or large corporate audits.

Revenue agents typically work with taxpayers who may have complex tax situations, including large businesses, corporations, or high-net-worth individuals. Their role is more analytical, focusing on the detailed examination of tax records rather than enforcement actions.

Authority and Enforcement Powers

Another key difference between revenue officers and agents is their level of authority and enforcement privileges.

Revenue Officer

Revenue officers have significant enforcement powers, enabling them to collect tax debt. They can place liens on a taxpayer’s property, levy bank accounts and garnish wages, and seize assets, including property, vehicles, and other valuables. They can also summon taxpayers to provide documentation or appear for interviews.

These enforcement powers make revenue officers one of the more intimidating figures within the IRS, as they have the authority to directly impact a taxpayer’s financial situation if taxes remain unpaid.

Revenue Agent

Revenue agents, while they do not have the same enforcement powers as revenue officers, have the authority to determine whether additional taxes are owed. They can propose changes to tax returns, leading to increased tax liabilities. They can also assess penalties and interest for underpayment of taxes and refer cases to revenue officers or the IRS Criminal Investigation division if they uncover significant fraud or evasion. The role of a revenue agent is more focused on the accurate calculation of taxes owed rather than direct collection.

However, the findings of a revenue agent can lead to subsequent enforcement actions by revenue officers if unpaid liabilities are identified.

Interaction with Taxpayers

The level of interaction with taxpayers also differs for revenue officers and agents.

Revenue Officer

Revenue officers often engage in direct, face-to-face interactions with taxpayers. They may visit a taxpayer’s home or business to discuss unpaid taxes, gather information, and collect payments. These interactions can be stressful for taxpayers, especially when enforcement actions are imminent. However, revenue officers also work with taxpayers to set up payment plans or resolve tax debts through negotiation.

Revenue Agent

Revenue Agents generally interact with taxpayers through audits, which may take place in person, over the phone, or by correspondence.

The audit process can vary in complexity, from simple correspondence audits handled by mail to more extensive field audits, where the revenue agent reviews records on-site. The interaction is usually more analytical and less confrontational than that of a revenue officer.

Impact on Taxpayers

Because of the level of authority, there is also a difference in the amount of impact these two figures hold on taxpayers.

Revenue Officer

The impact of a revenue officer on a taxpayer can be immediate and severe. If a taxpayer fails to cooperate or resolve their tax liability, the revenue officer can take enforcement actions such as levies or asset seizures, which can have significant financial consequences.

Revenue Agent

The impact of a revenue agent is more related to the accuracy of tax reporting. An audit by a revenue agent can result in additional taxes owed, along with penalties and interest.

However, revenue agents do not directly enforce collection, so the immediate financial impact may be less severe compared to that of a revenue officer.

Taxpayer Rights

When dealing with revenue officers and revenue agents, taxpayers have specific rights designed to protect them throughout the process. The IRS must inform taxpayers of these rights, including the right to be treated fairly, privacy, and representation. Taxpayers can seek the assistance of a tax professional, such as a certified public accountant (CPA), enrolled agent, or tax attorney, who can represent them in discussions with the IRS. Additionally, taxpayers have the right to appeal decisions made by revenue officers or revenue agents if they believe the IRS has made an error.

Understanding and exercising these rights can help ensure that interactions with the IRS are conducted fairly and according to the law.

How to Prepare for a Meeting with an IRS Revenue Officer or Agent

When the IRS contacts you, your response should be strategic and measured. Consider using these steps to guide your initial actions, whether you are dealing with a Revenue Agent or a Revenue Officer.

1. Identify the Purpose (Audit vs. Collection)

- Revenue Agent (Audit): The purpose is verification.

They are questioning the accuracy of your tax returns. Your goal is to prove compliance with documentation.

- Revenue Officer (Collection): The purpose is enforcement. They are seeking payment for delinquent taxes. Your goal is to negotiate a payment arrangement or settlement.

2.Gather Specific Documentation

Do not send generic records. Gather only the precise documents relevant to the IRS’s inquiry:

- For Audits (Agent): Collect specific tax returns, W-2s, 1099s, receipts, invoices, and bank statements directly supporting the deductions or income being examined.

- For Collections (Officer): Gather documentation of your current financial condition, including monthly expenses, income, and asset values (Form 433-A or Form 433-B), needed for negotiating a payment plan.

3. Consider Professional Representation

A tax resolution specialist (Tax Attorney, CPA, or Enrolled Agent) can officially represent you, allowing you to avoid direct interaction with the IRS. Representation is crucial to protect your rights, ensure legal compliance, and negotiate the best possible outcome.

4.Advice on Conduct During Meetings

If you must attend a meeting, your conduct is vital:

- Stay Calm and Professional: Maintaining a respectful demeanor facilitates a smoother process.

- Don’t Volunteer Information: Only answer the specific questions asked; do not offer excuses or provide information outside the scope of the inquiry.

- Let Your Representative Speak: If you hire a tax professional, all substantive communication should flow through them.

Tax Help for Those with a Revenue Officer or Agent

In summary, revenue officers are primarily involved in the collection of unpaid taxes and have significant enforcement powers. In contrast, revenue agents focus on auditing tax returns to ensure compliance with tax laws, with their work being more analytical and less enforcement driven. Contact from either professional indicates a serious matter that often requires expert representation.

The decision to seek professional tax representation is important. You should immediately consider legal representation if you are facing any of the following situations:

- You’ve been contacted by a Revenue Officer: This indicates an active collection case involving serious enforcement actions (liens, levies, or seizures).

A tax attorney can help negotiate payment plans or settlements and protect your assets.

- You’ve been notified of an Audit by an Agent: A formal audit by a Revenue Agent often requires complex document review and legal interpretation of tax laws. A professional can handle all communication, ensuring you only provide necessary information.

- You owe a significant amount of back taxes: Large liabilities require sophisticated strategies like an Offer in Compromise (OIC) or setting up installment agreements.

- You suspect or are accused of tax fraud or evasion: If the Revenue Agent refers your case to the Criminal Investigation division, you need a Tax Attorney immediately.

Optima Tax Relief is the nation’s leading tax resolution firm with over a decade of experience helping taxpayers with tough tax situations.

If You Need Tax Help, Contact Us Today for a Free Consultation

Disclaimer: This story is auto-aggregated by a computer program and has not been created or edited by finopulse.

Publisher: Source link